Every choice of what to do with Greece's foreign debt will have a price for local banks, which are theoretically prepared for some of the scenarios. Yet the question remains about the differences that will follow the theoretical scenarios and the reality.

Shortly before the secret meeting in Luxembourg, the disclosure of which put a lot of fuss about the Greek debt, an impression was widespread - in Athens, but also internationally – that the rescheduling of the debt was agreed upon and an opportunity was sought in order to make it official. An information reached the journalistic community that although the reserved position of some European governments, the notion of the deadline extension of the Greek debt was initially agreed upon.

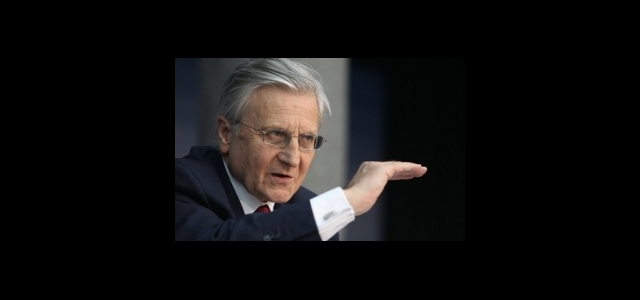

The only one, who expressed the opposite view from this general consensus, supported even by the "hardheaded" Germans, was Jean-Claude Trichet. Rumors even had it that his opposition was so strong that many believed that the message for the rescheduling of the debt will be issued only after Trichet leaves the European Central Bank at the end of October.

And all this before the meeting in Luxembourg, when the international markets had shaped a "sense for the fore coming”, for which had helped the rating agencies and also the media. For example, shortly after Easter in an article Bloomberg argued that the restructuring of the Greek debt is now overdue, and that Greece must declare a cut of its debt by around 50 percent and should announce a three-year deferral of payment of interest on outstanding loans. An article by the Economist pointed out a needed cut of 45 percent of the Greek debt.

In its report, JP Morgan foresaw a cut of 40 of the Greek debt. According to Citigroup a 42 percent cut was necessary while Deutsche Bank provided 50 percent with the proviso that this is necessary in order for the Greek debt to remain viable for a long period of time. Bank of America / Merrill Lynch found it probable the choice to cut the Greek debt within the range of 30 percent and Credit Suisse argued that Greece must remove 30 to 40 percent of its debt.

These were some of the "informed" assessments that raised the issue of restructuring the debt in the center of discussions. And except for the "bad" Trichet, the only person from the lobby in Brussels, who publicly declared his opinion against the already wide spread opinion, was the head of the European Financial Stability Fund (EFSF), Klaus Regling, who in an interview for the German Handelsblatt, argued that banks intentionally keep up the discussion about the restructuring of the Greek debt because they are expecting higher profits from the favorable conditions that would accompany it. As Regling mentioned, the European credit institutions recognize that they will suffer losses from the restructuring of the debt, however, they believe that the benefits they would receive are "much more promising." They also believe that any losses in their wallets will be limited. According to Regling by analyzing the conditions that come with restructuring of public debt in Latin America and Asia over the past two decades, banks have found that it took place with "high guarantees, which they would like to see in Europe as well with great pleasure”. This is why, says Regling, banks start the discussion of continuous debt restructuring.

After the meeting in Luxembourg, and the reactions that followed, it is clear that in the situation in which we find ourselves, the priorities have changed, said in an analysis the on-line magazine Banker's Review. Naturally the preceding discussion was not forgotten, but now the focus is on the problematic Trichet and the redundancy associated with the efficiency of the Greek government. The European Central Bank went so far as to threaten that if a restructuring of the debt happens, it will not accept Greek bonds to provide liquidity, which in reality closed the cash flow to Greek banks and at the same time set a ceiling on domestic credit and Greece! In more detail, from July 1, banks will not be able to receive as much cash as they want against a collateral of interest bonds from member countries of the euro zone, because an upper limit was adopted, which corresponds to the average of their lending over the past four months.

Clearly, this decision mainly affects Greece. The European Central Bank "saw" that in recent months the government has slowly but steadily increased the amounts received from issuance of bonds interest. Especially during the last two months the domestic credit grew enormously. In order to finance the primary deficit increases due to the failure of the budget, in April the state resorted to increase of borrowing by issuing quarterly and semi-annual interest bonds.

So, the decision of the European Central Bank targets the termination of this tactic. Jean-Claude Trichet and other European partners of Greece, who are quite reserved towards a possible restructuring of the debt, said to the Greek government that it is obliged to focus on strict enforcement of the budget. That is, it must first implement the reforms, privatization, a "convincing" program to squeeze public spending, and that everything else will come afterwards. Moreover, says the European Central Bank, the banking system is unable to finance the ever-growing credit needs of the country at a time when the uncertainty due to failure in achieving the goals "eats" all the deposits.

{kind=link}